AESO – Deferral Account Shortfall

In this decision, the AUC approved the request from the Alberta Electric System Operator (“AESO”) to settle its 2019 net deferral account shortfall with market participants, of $41.6 million.

Introduction and Application Details

In July 2020, the AESO filed its application for approval of its 2019 deferral account reconciliation (“DAR”) and for changes to the deferral account balances for 2018 to 2012. The deferral account balance resulted from differences between costs the AESO had incurred in providing system access service (“SAS”) and the revenues recovered in rates charged to market participants in prior periods. The AESO requested approval of its determination and allocation of a $41.6 million net deferral account shortfall.

The AESO also requested approval to settle the amounts for the 2019 deferral account balance on an interim and refundable basis, subject to adjustment in the final decision to facilitate immediate settlement of the deferral account amounts with market participants.

Methodology, Allocation and Settlement of Deferral Account Balances

The AESO noted that this application relied on the approval granted by the AUC in Decision 22942-D02-2019 to apply the revised DAR methodology for production years 2017 and onward.

The AESO explained that the allocation of deferral account balances and adjustments were implemented through its continued use of a software program that it developed to calculate DARs. This approach was consistent with its previous DAR applications.

The AESO submitted that after the allocation of deferral account balances is determined by rate and rate component for each market participant, additional revenue already settled through Rider C or in prior DARs with each market participant would be subtracted or added by rate and rate component. The remaining balance would be the amount of the deferral account charge or refund attributed to the market participant on a production month basis, by rate and rate component.

The AESO proposed to settle the outstanding deferral account balances through a one-time payment and collection option and, similar to past reconciliation applications, it offered a three-month payment option, including carrying charges, if the one-time payment option presented a financial burden to market participants.

AUC Findings

The AUC reviewed the AESO’s methodology and found that it is consistent with the methodology approved for DAR applications in Decision 22942-D02-2019. It also reviewed the allocation of the deferral account balances and found that it is consistent with previously approved DAR applications and with the 2018 ISO tariff. The AUC approved the AESO’s methodology, allocation and settlement of the deferral account balances.

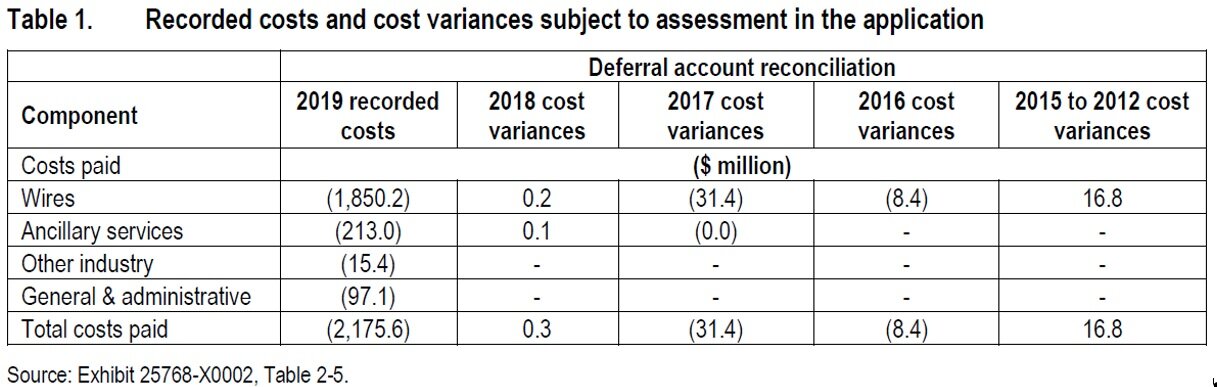

Cost Variances

The AUC noted that this application represented the first opportunity to consider the actual, recorded AESO revenue requirement costs for the year 2019, and the first opportunity to consider cost variances for the years 2018 through to 2012 concerning the recorded cost amounts for those years, after the AUC’s assessment in Decision 24910-D01-2019. The costs and cost variances applied for in the application were summarized in Table 1 below:

As set out by the AUC in Decision 2014-242, there are four principal categories of costs and expenses incurred by the AESO in its tariff:

AESO’s Administrative Costs and Ancillary Costs

No issues were raised by interested parties regarding the AESO’s own administrative costs or its ancillary costs. The AUC accepted these costs as submitted by the AESO.

Transmission Line Losses

The AESO did not include the reconciliation of transmission line loss amounts in the application. This is consistent with the approach taken in previous DAR applications, given that effective January 1, 2006, the cost of transmission system losses was no longer subject to the retrospective DAR.

Costs Related to Transmission Wires Payable Under a TFO Tariff

Regarding transmission facility owner (“TFO”) wires-related costs and cost variances, the AUC found that the AESO must pay the rates set out in the approved tariff of the owner of each transmission facility according to Section 32 of the Electric Utilities Act (“EUA”). The AUC approved the costs and expenses of a TFO in the TFO’s applicable tariff application, according to Section 122 of the EUA. The costs and cost variances submitted by the AESO for TFO wires-related costs were approved as filed.

Deferral Account Amounts

The AESO identified a net shortfall of approximately $41.6 million (net of Rider C charges and refunds, and any prior DAR settlements) to be allocated to customers, composed of the following amounts:

The AUC accepted the accuracy of deferral account amounts and the calculation of the net deferral account shortfall of $41.6 million. The AUC approved the deferral account balances and the net deferral account shortfall amount of $41.6 million.