Rates – True-Up – Transmission Access Charge

In this decision, the AUC considered an application by FortisAlberta Inc. (“Fortis”) requesting approval of its 2018 annual transmission access charge deferral account (“TACDA”) true-up and carrying costs on the true-up amounts in accordance with Rule 023: Rules Respecting Payment of Interest. The AUC approved the 2018 TACDA true-up net refund amount of $27.033 million as filed, by way of a base 2020 transmission adjustment rider (“TAR”) to be in effect from January 1, 2020, to December 31, 2020 (“2020 TAR”).

The AUC also considered Fortis’s proposal to modify the application of the quarterly transmission adjustment rider (“QTAR”) as applied to irrigation customers (Rate 26) and the presentation of quarter-over-quarter bill impact analysis for these customers. The AUC accepted Fortis’s proposal to set the QTAR for irrigation customers to zero in Quarter 1 (Q1) and Quarter 4 (Q4) as energy usage by irrigation customers is minimal during these periods. It also accepted Fortis’s proposal to use previous year quarterly result comparators as a basis for completing quarter-over-quarter bill impact analysis when that comparator is more relevant than the previous quarter from the current year.

Background

Fortis filed its application on August 16, 2019.

All electric distribution companies (“DFOs”) accessing the electric transmission system in the province are charged by the Alberta Electric System Operator (“AESO”) for transmission services provided in relation to customers in their distribution service areas. The purpose of Fortis’s annual TACDA true-up application is to ensure that the revenues collected through its transmission access charges in a year recover the AESO tariff charges that Fortis pays to the AESO in that year.

Details of the Application

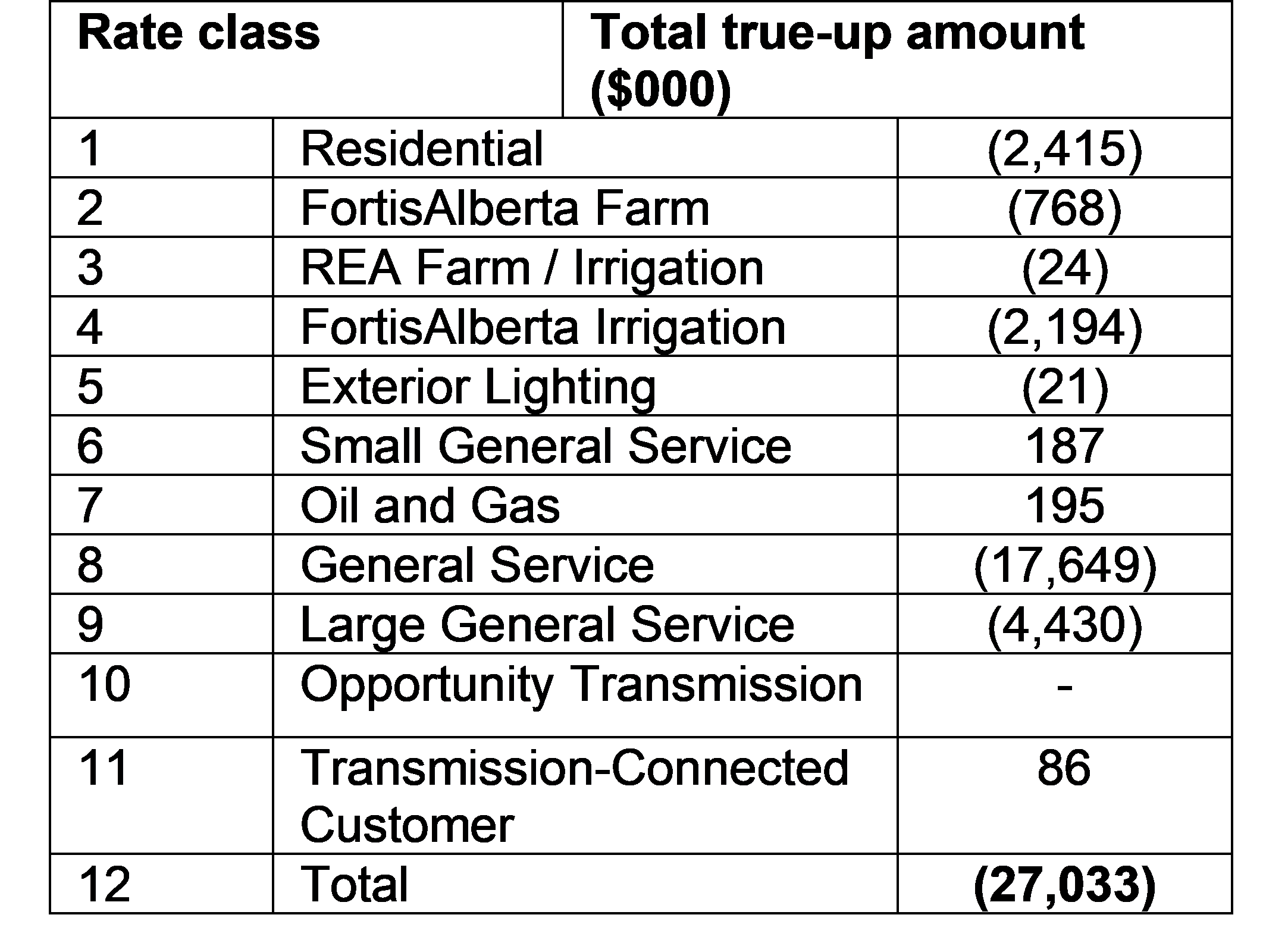

Fortis applied for a net 2018 TACDA refund to customers of $27.033 million. The allocation of this net refund amount to customer rate classes, as proposed by Fortis, is set out in the following table.

Calculation of the True-Up Amount

The components of the 2018 TACDA true-up included the true-up of a 2016 rider related to the AESO charges, and the true-up of the four amounts arising from the various 2018 AESO charges. This included the system access service (“SAS”) deferral true-up, AESO deferral account reconciliation (“DAR”) true-up, Balancing Pool true-up and border customer deferral account true-up, as well as carrying costs associated with those amounts.

TACDA Rider True-Up

The AUC noted that the purpose of a deferral account rider true-up is to ensure that, for each of the AESO charges, the amounts actually collected or refunded equal the amounts approved by the AUC. Fortis calculated the amount of the rider true-up as the difference between the 2016 annual TACDA true-up refund of $30.416 million, approved in Decision 22883-D01-2016, and the actual amount refunded of $31.297 million, resulting in the true-up of $0.881 million on an aggregate basis.

SAS Deferral True-Up

The AUC noted that the purpose of a SAS deferral true-up is to reconcile the actual transmission access revenue received from customers to the actual transmission access costs paid to the AESO. Fortis indicated that its 2018 actual transmission access costs, excluding transmission costs for transmission-connected Rate 65 customers, were $621.708 million, while its actual transmission access revenues for distribution connected customers, including revenues received through its quarterly TACDA riders, were $636.336 million. Fortis, therefore, applied to refund $14.628 million to customers.

AESO DAR True-Up

Under section 14(3) of the Electric Utilities Act, “The Independent System Operator must be managed so that, on an annual basis, no profit or loss results from its operation.” Accordingly, any variances arising between the actual costs the AESO incurs and the forecast amounts, recovered through its rates based on forecast volumes, are refunded to or recovered from market participants by way of the AESO DAR, typically undertaken on an annual basis. In turn, the DFOs flow through these collections or refunds to customers in their service areas.

In Decision 23802-D02-2018, the AUC approved the AESO’s 2016 DAR. Fortis was refunded $16.884 million. Of this amount, $5.08026 million was refunded to transmission-connected service Rate 65 customers, while Fortis applied in this application for the remaining balance of $11.804 million to be refunded to distribution connected customers.

Balancing Pool True-Up

The AUC noted that the purpose of Fortis’s Balancing Pool true-up is to ensure that its Balancing Pool refund to or collection from its customers matches its settlement with the AESO. In 2018, Fortis paid $55.483 million to the Balancing Pool. Due to differences between forecast and actual billing determinants (also known as billing units – in this case, energy flowed through Fortis’s distribution system), Fortis collected $55.660 million from its customers in 2018, necessitating a net refund of $0.178 million.

Border Customer Deferral

Border customers are customers in Fortis’s service area that receive energy through a connection to a distribution or transmission system located outside Alberta. The purpose of the border customer deferral account is to capture the net differences between Fortis’s receipts and payments pertaining to transactions related to the extra-provincial supply of energy and wires services to border customers in accordance with Section 16 of the Isolated Generating Units and Customer Choice Regulation.

Fortis indicated that in 2018, the total payments pertaining to service to its border customer suppliers were $0.658 million, while the receipts from the Power Pool were ($0.382) million, resulting in a collection of $0.276 million.

Carrying Costs

Fortis calculated carrying costs on outstanding amounts related to the true-up balances in accordance with Rule 023. The total carrying costs amounted to a net refund of $1.580 million.

AUC Findings

The AUC approved a net refund of $27.033 million, as calculated by Fortis in its application and the resulting true-up amount for each rate class.

2020 TAR

Fortis proposed to refund the 2018 TACDA true-up amount by way of the base 2020 TAR to be applied over the 12-month period from January 1, 2020, through to December 31, 2020.

In the application, Fortis did not calculate its 2020 TAR rates as it did not have the forecast base 2020 transmission access charges, which would be determined in its 2020 annual PBR rate adjustment filing. Fortis subsequently included the 2020 TAR percentages, calculated as part of its 2020 annual PBR rate adjustment filing.

The AUC noted that the 2020 TAR percentage rate would be determined in Fortis’s 2020 annual PBR rate adjustment filing in proceeding 24876.

Rider C Analysis

Based on the Rider C analysis provided, the AUC found that converting the approved percentage based Rider C rates to the equivalent $/MWh charge remains appropriate in the calculation of the AESO Rider C allocation.

Irrigation Rate Class QTAR Proposal

As part of the application, Fortis included a proposal to make adjustments to the application of the QTAR mechanism in 2020; specifically, Fortis proposed to make adjustments to the way the rider is applied to irrigation rate class customers (Rate 26) and the presentation of the quarter-over-quarter bill impact analysis. Fortis proposed that the “Q1 and Q4 QTAR rates for the Irrigation rate class (Rate 26) be set to $0/MWh and not used in the quarter-over-quarter bill impact comparison in the respective Quarterly AESO DTS Deferral Account Applications.” Fortis explained that the proposed change, “is a result of the seasonality of the irrigation season and QTAR rate being collected on the majority of the energy from April 1 to October 31 with minimal energy being consumed by the irrigation rate class during Q1 and Q4.”

The AUC found the Fortis proposal reasonable and approved its use in future QTAR applications.